Sometimes identifying the best stocks to buy can be difficult, but you could do a lot worse than checking out the stocks selected by one of the world’s savviest hedge fund managers – Warren Buffett.

Buffett’s stock picks are a popular source of inspiration for investors, and for good reason. His formidable stock-picking ability has given him the nickname ‘the Oracle of Omaha’ and a fortune of ~$117 billion, making him one of the richest people in the world. His firm, Berkshire Hathaway, is also counted among the most successful, boasting total assets of over $1 trillion.

So obviously when Buffett goes shopping, investors are keen to find out what’s in the bag. During Q2, Buffett opened new positions in a few homebuilding stocks, and as he is known for his value investing style, he must think these names offer just that right now.

But it’s not just Buffett who likes the look of these particular equities. Raymond James analyst Buck Horne has also pinpointed an opportunity in these stocks, believing they are primed to deliver double-digit growth over the next year.

For a fuller view of their prospects, we decided to run these tickers through the TipRanks database. Here’s what we found.

D.R. Horton, Inc. (DHI)

The first stock Buffett is betting on is D.R. Horton, a Texas-based construction firm and a leader in the US homebuilding industry. The company has held the title of the ‘nation’s largest homebuilder’ for more than 20 years and operates in 113 residential markets across 33 states. D.R. Horton works on projects for both single-family homes and multi-family apartment complexes.

D.R. Horton has been building homes for 45 years, and has closed over 1 million building contracts in that time. The company has a portfolio of designs, featuring homes in all price brackets, from under $200,000 to over $1 million, and can even implement smart home technology from ground up during construction.

While the company holds a leading position in its industry, it has felt the effects of real estate headwinds. Earnings are down year-over-year for the past several quarters, even as revenues have showed y/y gains. This pattern continued in the recently reported results for Q3 of fiscal 2023. DHI had a top line of $9.7 billion, up 11% from the year-ago quarter, but the bottom line non-GAAP EPS of $3.90 was well below the 3Q22 figure of $4.67. That said, of greater import for investors, DHI beat the forecasts at both the top and bottom lines in Q3, with revenue coming in $1.31 billion above expectations and EPS beating by $1.07 per share.

Looking forward, DHI reported two important metrics that bode well for future business. First, it closed on 22,985 homes in Q3, a year-over-year increase of 8%, and the total value of those homes closures was up 4% y/y, to $8.7 billion. And, the company’s net sales orders were up an impressive 37% y/y, to 22,879 homes. The total value of the net sales orders was reported as $8.7 billion, for a 26% y/y increase. As such, the company raised its revenue outlook for the year, with the top-line now expected to hit the range between $34.7 billion to $35.1 billion compared to $31.5-$33 billion beforehand. Consensus had $32.34 billion.

As for Warren Buffett, his firm opened a new position in DHI during the calendar second quarter. Berkshire Hathaway disclosed total purchases of 5,969,714 shares of DHI, a major stock acquisition that is now worth about $700 million.

Turning to the Raymond James view, we find that analyst Buck Horne is impressed with D.R. Horton’s prospects for the next few quarters. He writes, “As it stands, we now see DHI on a path toward double-digit EPS growth and 20%+ ROIC metrics in FY24, most notably supported by a surging rental housing platform – which we think will significantly mitigate cyclical volatility associated with mortgage rates. With its pristine balance sheet primed for growth and acquisition opportunities, we believe DHI’s earnings visibility and profitability have improved to the point that investors should not be afraid of current valuations.”

Alongside these comments, Home gives DHI shares an Outperform (i.e. Buy) rating, with a price target of $160 that implies a one-year upside potential of ~36%. (To watch Home’s track record, click here)

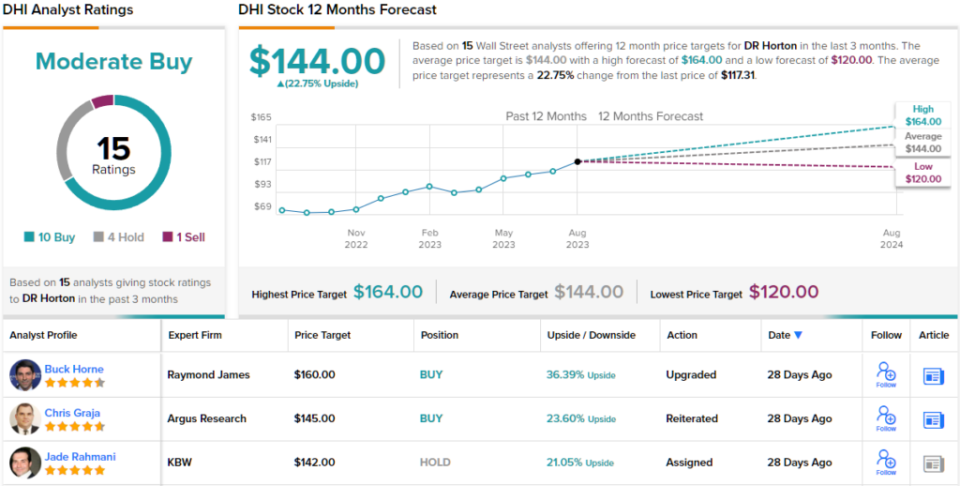

Overall, DHI has picked up 15 recent Wall Street analyst reviews, and these include 10 Buys, 4 Holds, and 1 Sell to give the stock its Moderate Buy consensus rating. The shares are selling for $117.31 and the $144 average price target implies ~23% upside on the one-year horizon. (See DHI stock forecast)

Lennar Corporation (LEN)

The next Buffett choice we’re looking at is Florida-based Lennar Corp, another of the major homebuilders in the US. Lennar operates on the East Coast and Southeast, in the Great Lakes region, in Texas and Oklahoma, and in the West and West Coast regions. The company is perennially among the top 5 largest homebuilders in the country, counting by total home sales. Since its founding in 1954, Lennar has built more than 1 million homes.

The company controls a number of brands, that offer services in all aspects of the new-home industry. There are five brands operating on the construction side, while Lennar Mortgage, Lennar Title, and Lennar Insurance Agency provide the necessary financial services to make the homes available to buyers. Lennar has a long history of expanding its operations through acquisition, and currently works in 26 states.

In 2022, Lennar reported more than $33 billion in total revenues, but the company is not quite on track so far this year to meet that figure. In its 2Q23 report, Lennar showed a top line of $8.05 billion, down 3.7% y/y, although it should be noted that was some $810 million above the estimates. The company’s Q2 earnings, an EPS of $2.94 by non-GAAP measures, also beat the forecast – by 62 cents per share.

Lennar delivered 17,074 homes in Q2, and finished the quarter with new orders for 17,885 homes – worth a total of $8.2 billion. The company’s work backlog, an important metric for future business, was reported at 20,214 homes, valued at $9.5 billion.

Reflecting a new position for Buffett’s Berkshire Hathaway, the firm pulled the trigger on 152,572 shares in Q2. This stake in Lennar is currently valued at $17.85 million.

Also bullish on this stock, Raymond James’ Buck Horne is impressed by Lennar’s ability to maintain production.

“Combining targeted price reductions, incentives, and mortgage rate buydowns to keep home production flowing, despite mortgage rate volatility, Lennar has been able to identify the remarkable reservoir of pent-up housing demand much sooner than most… We find shares of LEN trading at 1.7x trailing book value and 9.5x our FY24 EPS, roughly in line with peer averages. As such, we think LEN shares remain worthy of a material valuation re-rating thanks to a 15%+ projected ROIC, double-digit EPS growth, and a net debt free balance sheet,” Horne opined.

Quantifying his stance, Horne goes on to rate LEN an Outperform (i.e. Buy), and he puts a $150 price target on the stock to show his confidence in a 28% gain on the 12-month horizon.

All in all, Lennar has picked up 16 recent analyst reviews, and these include 10 Buys, 4 Holds, and 2 Sells to give the stock its Moderate Buy consensus rating. The average price target of $134.40 and the current trading price of $117 together point toward ~15% one-year upside potential. (See Lennar stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.