“What lies ahead for the stock market?”

That’s the burning question on the minds of every market and economic expert out there, and it’s undoubtedly a challenging one.

Inflation has moderated to a reasonable 3% annually, and the job market is showing signs of strength. Stocks are surging, indicating that investors have factored in the risk of a potential recession. However, this leads to a problem highlighted by B. Riley’s chief investment strategist, Paul Dietrich. He points out that the latest earnings figures are lagging far behind the surging positive sentiment. This discrepancy between market optimism and lukewarm earnings could spell trouble for investors.

“It doesn’t take a stock market historian to know that something terrible will happen when the stock market surges and the S&P 500 companies’ earnings decline -6.8% in Q2 2023,” Dietrich opined. “According to FactSet, the quarter will mark the most significant earnings decline reported by the index since Q2 2020 when the Covid pandemic closed down the country. This was the third consecutive straight quarter of year-over-year earnings declines. That is officially an ‘earnings recession.’”

As Dietrich sees it, the decline is real and its only a matter of time before it impacts sentiment and investing activity.

A cautious approach would naturally pull investors toward dividend stocks, the classic defensive play. Dividends offer a steady, passive income stream, providing investors with a degree of protection – and usable cash – for an uncertain market environment.

Following this cue, B. Riley’s 5-star analyst, Bryce Rowe, is going bullish on two dividend stocks in particular. These dividend payers offer high yields of 9% or more and present compelling investment theses. Let’s take a closer look.

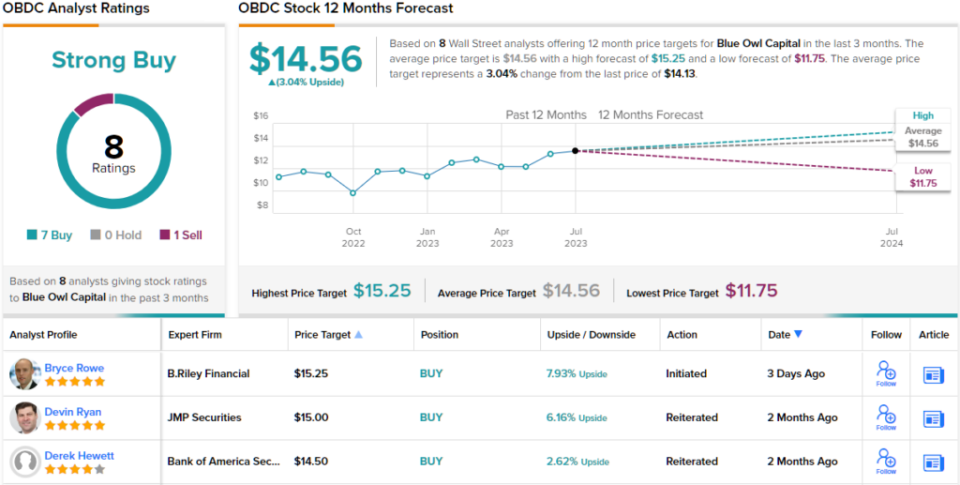

Blue Owl Capital Corporation (OBDC)

First up is Blue Owl Capital, a business development corporation operating under the umbrella of the larger Blue Owl Capital asset manager. Formed in the first half of 2021 through a SPAC merger between Owl Rock and Dyal Capital with Altimar Acquisition, the new firm has been shifting its branding to the Blue Owl name earlier this month.

Under the Blue Owl branding, the business development corporation gets a new ticker and a place in the larger Blue Owl organization, while retaining its existing BDC portfolio and historical financial records. Like its BDC peers, Blue Owl Capital Corporation invests in small- and mid-sized business enterprises, providing access to capital for firms that have difficulty entering the traditional banking system. The company’s portfolio contains 187 companies and boasts a fair value of $13.2 billion. The portfolio is made up of 85% senior secured investments, and 98% is in floating rate debt investments.

The company will release its 2Q23 financial results on August 9, but we can look back at Q1 to see where Blue Owl stands now. The top line, of $377.6 million, was up almost 43% year-over-year and beat the forecast by $12.7 million. At the bottom line, the company’s non-GAAP EPS figure was 45 cents per share, showing a 45% growth compared to the previous year and beating the estimates by 2 cents per share.

Financial results are not the only data point that Blue Owl inherited from the old Owl Rock name; the company also retains its dividend history. The last dividend payment, declared on May 10 for a July 14 payout, was set at 33 cents for the regular quarterly common share payment, including a 6 cent irregular payment. The company’s regular dividend annualizes to $1.32 per common share and yields 9.34%; it has added an irregular dividend payment in each of the last three quarters.

Turning to the B. Riley view, as articulated by top analyst Bryce Rowe, we find that he is impressed by Blue Owl’s combination of low share price, solid dividend, and strong business. In Rowe’s words, “We see the risk/reward profile as favoring reward given our view of limited downside potential with a discounted valuation, the supportive earnings environment, healthy dividend coverage, and the size and scale of Blue Owl’s direct lending platform that we believe should allow the company to take advantage of the ongoing shift from more traditional financing sources to private debt. Based on $1.59/share of projected regular and supplemental dividends (3Q23– 2Q24), Blue Owl Capital trades with an ~11% dividend yield and at 92% of NAV.”

Rowe goes on to give Blue Owl stock a Buy rating, while his $15.25 price target suggests an 8% upside for the year ahead. Based on the current dividend yield and the expected price appreciation, the stock has ~17% potential total return profile. (To watch Rowe’s track record, click here)

Overall, Blue Owl Capital Corporation has picked up 8 recent Wall Street analyst reviews, including 7 to Buy and 1 to Sell, for a Strong Buy consensus rating. (See OBDC stock forecast)

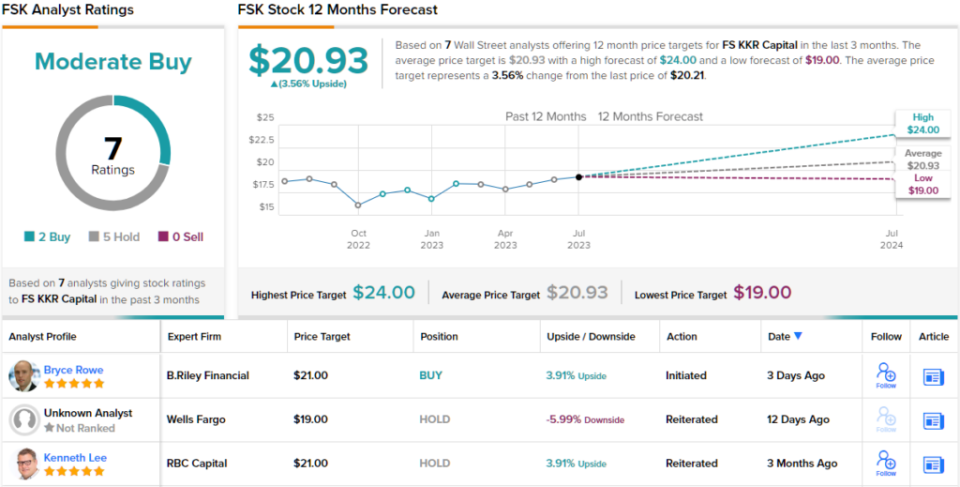

FS/KKR Capital Corporation (FSK)

Next up is FS/KKR, another business development corporation working with private middle market firms in the US small business sector. FS/KKR focuses mainly on senior secured debt and has a lesser interest in subordinated debt, with a long-term goal of providing the best possible risk-adjusted returns for its investors.

FS/KKR has put an overwhelming majority of its portfolio into senior secured debt, accounting for 69% of the total. Of the debt investments, 89% are floating rate. FS/KKR has investments in 189 companies, with a median company earnings of $114 million as of the end of Q1. By fair value, this BDC’s portfolio is worth $15.3 billion.

When we turn to the company’s financial results, it’s clear that FS/KKR can generate a profit even while revenues appear shaky. Over the past few years, the top line has been volatile while earnings have shown a modest increase. The last reported quarter was 1Q23, and the firm’s top line, total investment income, came in at $456 million, a figure that was up 15% year-over-year and $11.56 million ahead of forecasts. The bottom line EPS, in non-GAAP terms, was 81 cents per share, which was 6 cents per share better than had been estimated.

Even better for dividend investors, this company’s bottom line provides full coverage for the regular dividend. In the Q1 report, FS/KKR declared a total dividend payment of 70 cents per common share. This included a 64 cent base payment and a 6 cent supplemental distribution, and it was paid out earlier this month. Taken together, the 70 dividend annualizes to $2.80 and gives an impressive yield of 13.85%. Along with this high dividend payment, FS/KKR also declared a 15 cent special distribution, with the payment scheduled in three tranches of 5 cents each: one in May, one at the end of August, and one at the end of November.

Checking in with Bryce Rowe, we find the B. Riley analyst taking an upbeat view of this stock, and giving particular note to the earnings support for the high dividend, and the company’s likely ability to maintain that payment going forward. Rowe writes of FS/KKR, “We see the risk/reward profile as favoring reward given the deep P/NAV discount that should likely limit downside, the supportive earnings backdrop, a dividend yield of [approximately] 14% based on projected dividends 3Q23-2Q24, an attractive capital structure, sufficient liquidity, and FSK’s positioning to benefit from borrowers shifting from more traditional sources for financing solutions to private debt providers.”

Taking his stance forward, Rowe rates FSK stock a Buy, with a $21 price target pointing toward a roughly 4% upside on the one-year horizon. The real attraction for investors here is the strong dividend yield.

Overall, FSK gets a Moderate Buy rating from the consensus of Wall Street analysts, based on 7 recent reviews that break down to 2 Buys and 5 Holds. (See FSK stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.