Some people’s exploits in their chosen profession transcend beyond the industry they operate in – making them household names. It’s pretty safe to claim that even those not interested in the investing world are familiar with Warren Buffett.

Buffett embodies the term ‘legendary investor’ probably more than any other and considering his decades of almost unrivalled stock picking success, it’s a thoroughly deserved epithet.

For those looking to emulate a fraction of Buffett’s success, get ahead of the game, it makes sense to see which stocks currently reside in the Oracle of Omaha’s portfolio. And when some of those equities also have the support of one of Wall Street’s leading banks, such as Goldman Sachs, it conveys an even stronger message that the time might be right for loading up.

Against this backdrop, we delved into the TipRanks database to get the lowdown on three stocks that currently get the endorsement from both Buffett and the banking giant. Let’s check the details.

Occidental Petroleum (OXY)

For our first Buffett/Goldman-backed name, we’ll turn to the energy sector and the multinational firm Occidental Petroleum. The Houston, Texas-based company engages in the exploration, production, and marketing of oil and gas. Active since 1920, Occidental has become one of the largest independent oil and gas producers in the United States. The company also operates globally, with significant activities not only in the US but also in the Middle East and Latin America.

With its know-how and global reach, the company benefited immensely from rising energy prices last year, and like many names in one of the few sectors to thrive, OXY stock had a stellar 2022 – notching gains of 117%. But its performance has been more muted this year.

Affected by reduced volumes and prices for crude oil, natural gas liquids, and domestic natural gas, in Q1, revenue fell by 14.9% year-over-year to $7.26 billion, missing the Street’s forecast by $110 million. Profits also dropped, with adj. EPS falling by 48% to $1.09, which came in shy of the $1.37 consensus estimate.

Although free cash flow fell by 33% in Q1 to $1.69 billion, that hasn’t halted the company’s stock buying activities. In the quarter, Oxy repurchased $752 million worth of stock, keeping it on track to meet its $3 billion repurchase program for 2023.

Despite the underperformance, to say Buffett remains an OXY fan is a bit of an understatement. OXY shares make up a bug chunk of his portfolio, and during Q1, Buffett purchased an additional 17,355,469 shares. Notably, he continued to demonstrate his faith in May by purchasing approximately 5.62 million more shares. As it stands, Buffett’s ownership of around 217.3 million OXY shares translates to a staggering $12.73 billion, representing an impressive 24.4% stake in the company.

Buffett’s unwavering faith in OXY is backed up by Goldman Sachs analyst Neil Mehta, who shares a positive view on the company. Mehta, a 5-star analyst, points out a few key reasons why OXY looks promising, noting: “We remain positive on OXY due to its attractive FCF generation potential (13% FCF yield vs. 9% for diversified peers), which can drive robust share repurchase and allow the company to redeem its preferred equity and simplify its corporate structure (a focus for the company this year). Our favorable FCF outlook is underpinned by above-mid-cycle cash flows from chemicals, and we continue to expect favorable upstream results from OXY’s Permian operations.”

These comments underpin Mehta’s Buy rating while his $77 price target makes room for 12-month returns of 31%. (To watch Mehta’s track record, click here)

Elsewhere on Wall Street, the stock garners an extra 7 Buys and Holds, each, for a Moderate Buy consensus rating. The forecast calls for one-year gains of 22%, considering the average target stands at $71.67. (See OXY stock forecast)

Charter Communications (CHTR)

Let’s now pivot from energy to a big player in the telecom industry. Charter Communications is one of the US’s largest telecommunications and mass media companies. In fact, by subscribers, it is the country’s second-largest cable operator. Charter provides a wide range of offerings including cable television, high-speed internet, and telephone services to residential and commercial customers. Operating under the brand name Spectrum, the company serves millions of customers across 41 states.

In addition to its core services, Charter has also ventured into the streaming market with its video-on-demand platform, Spectrum TV, which offers a broad selection of movies and TV shows to subscribers.

Despite missing expectations on the profit profile in last month’s 1Q23 report, investors seemingly preferred to focus on the positives. EPS of $6.65 missed consensus expectations of $7.50, but revenue grew by 3.4% year-over-year to $13.65 billion and surpassing the Street’s projection by $40 million. Furthermore, adjusted EBITDA increased by 2.6% from the same period a year ago to reach $5.4 billion. In the quarter, the company also reported a record of 686,000 wireless net adds.

As for Buffett’s involvement, he owns a chunk of CHTR stock. His total holdings of 3,828,941 shares are currently worth over $1.27 billion.

The telecom giant also gets the support of Goldman Sachs analyst Brett Feldman, who sees some shareholder pleasing moves ahead.

“We remain confident that CHTR can achieve LSD EBITDA growth in 2023, with growth accelerating in 2H23 as opex comps ease… We continue to expect that CHTR will be able to sustain, and gradually ramp, its share repurchases over the next 5 years, even during periods of elevated capex, based on our outlook for sustained EBITDA growth, which should create additional borrowing capacity that we expect CHTR to use to fund buybacks. As such, we estimate that over the next 5 years CHTR will repurchase nearly $40bn of stock representing almost 60% of its market cap,” Feldman opined.

Accordingly, Feldman rates CHTR shares a Buy rating along with a $450 price target. The implication for investors? Potential upside of 35% from current levels. (To watch Feldman’s track record, click here)

The Goldman Sachs view represents the bulls here; the Street shows a definite split in the reviews for CHTR. Out of 16 recent analyst reviews, there are 7 Buys, 8 Holds, and 1 sell, for a Moderate Buy consensus rating. Going by the $469.65 average target, investors will be pocketing returns of 41% a year from now. (See CHTR stock forecast)

Marsh & Mclennan Companies (MMC)

Now let’s shift gears once more to a globally recognized professional services company that has received endorsements from both Buffett and Goldman Sachs. Marsh & McLennan is a prominent player in the field, specializing in risk management, insurance brokerage, and consulting services. The company operates through its four main subsidiaries: Marsh, Guy Carpenter, Mercer, and Oliver Wyman. With expertise spanning these diverse sectors, Marsh & McLennan is well-positioned to deliver comprehensive solutions to its clients on a global scale.

Marsh provides insurance broking and risk management solutions to clients, helping them deal with complex risks while protecting their assets. Guy Carpenter focuses on reinsurance brokerage and strategic advisory services, assisting insurers in managing their reinsurance needs. Mercer specializes in human resources consulting, offering a wide range of services related to employee benefits, talent management, and retirement planning. Lastly, Oliver Wyman provides management consulting services, assisting clients in various industries with strategic planning, risk assessment, and operational improvement.

Being in business for more than 150 years, MMC has established itself as a trusted global name, and this was evident in the company’s most recently reported quarter – for 1Q23. Boosted by a strong display from its risk and insurance services, revenue climbed by 6.3% year-over-year to $5.9 billion, edging ahead of the forecast by $40 million. Adj. EPS of $2.53 improved on the $2.30 generated in the same period a year ago whilst also coming in $0.06 above Street expectations. During the quarter, the company bought back 1.8 million shares of its stock for $300 million.

Buffett enters the frame here via the 404,911 MMC shares he presently holds. At the current price, these are worth over $70.58 million.

The global services firm also has a fan in Goldman analyst Robert Cox. Scanning the Q1 print, Cox finds plenty of reassuring points to keep him on board.

“We view MMC 1Q23 results as further evidence that the company is taking advantage of strong P&C broking conditions, talent investments are producing results, and margins are set to continue expanding materially with further expense efficiencies identified,” the analyst explained. “The broad based RIS organic growth beat in the quarter combined with our expectations for modestly decelerating P&C pricing and exposure growth leads us to raise our FY23 RIS organic growth estimate by 50bps to +9.7% (+7.1% excluding fiduciary investment income).”

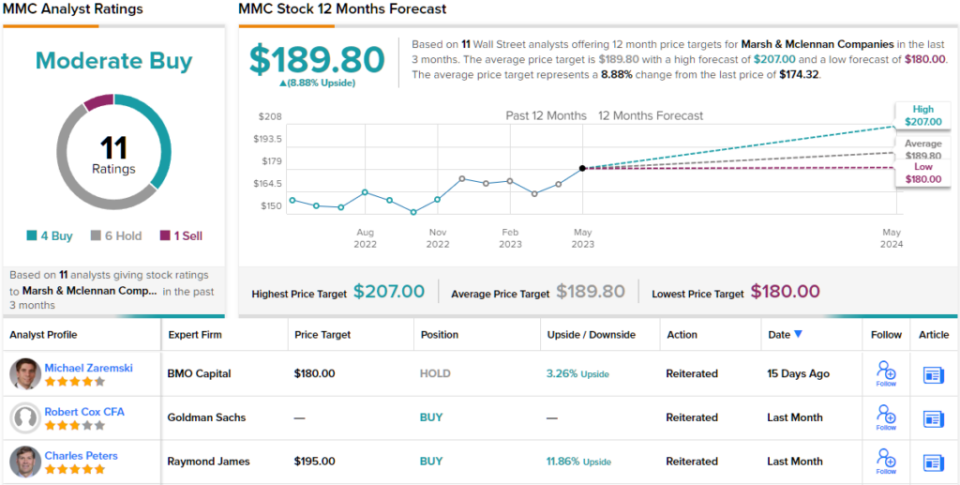

Putting these thoughts into grades and numbers, Cox rates MMC shares a Buy, backed by a $202 price target. Should the figure be met, investors are looking at upside of 16% from current levels. (To watch Cox’s track record, click here)

Looking at the consensus breakdown, 3 analysts join Cox in the bull camp and with an additional 6 Holds and 1 Sell, the stock claims a Moderate Buy consensus rating. At $189.80, the average target implies shares have room for ~9% growth over the coming months. (See MMC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.